The shock and its transmission to fertilizer markets

The outbreak of military conflict involving Iran, Israel, and the US in late February 2026 demonstrates how interconnected global energy, trade, and agriculture systems can amplify the effects of regional conflicts. While the war continues to evolve, its immediate consequences, including damage to infrastructure, restrictions on maritime navigation in the Persian Gulf, tighter sanctions, and heightened geopolitical uncertainty, have disrupted fertilizer supply chains.

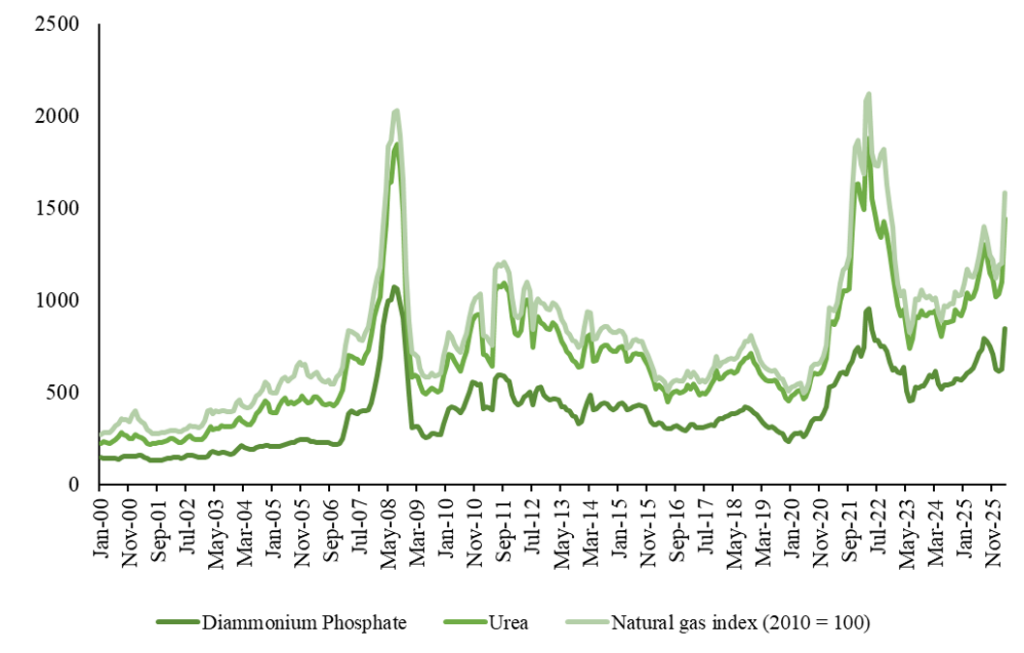

Fertilizer production is energy-intensive, with natural gas accounting for up to 70–80 percent of production costs for nitrogen-based fertilizers. The Persian Gulf is both a primary producer of these inputs and a critical transit hub. The Gulf Cooperation Council countries (GCC) and Iran together supply one third of global urea exports, and nearly half of traded sulfur . The closure of the Strait of Hormuz, a critical maritime chokepoint for global crude oil, liquefied natural gas (LNG), and fertilizers, has simultaneously disrupted production, feedstock supply, and export logistics, creating a compounding supply shock that propagated through agricultural systems.

Consequently, this regional conflict has quickly escalated into a global fertilizer supply crisis, with most immediate and acute consequences felt in agriculture-dependent economies, where access to energy, inputs, and trade routes is critical for food production and stability.

Why the MENA region is vulnerable to fertilizer supply shocks

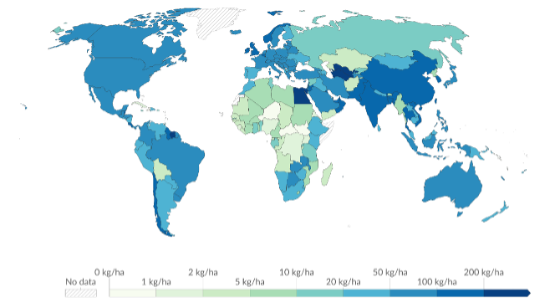

The Middle Eastern and North African (MENA) countries face inherent agricultural constraints that make them exceptionally vulnerable to global supply chain shocks with limited buffers against external disruptions. More than 80% of the region is arid or semi-arid, characterized by nutrient-poor, saline soils and severe water scarcity, forcing agricultural systems to rely heavily on energy-intensive irrigation and synthetic fertilizers (Figure 1). Dependence on nitrogen fertilizers is particularly acute in the region, as they must be applied every growing season to sustain yields. This creates a tight dependency between fertilizer availability and immediate production outcomes, meaning supply disruptions can reduce crop yields within a single season.